Realtor Rebate vs. Seller Concessions in Utah: 2026 Buyer’s Guide

What if you could walk away from your closing with a $5,000 check and zero out your closing costs? Most Utah buyers think they have to choose between a lower price and cash on hand. They are wrong. You can actually have both! Mastering the balance of a realtor rebate vs seller concessions utah is the ultimate power move in today’s market. With average mortgage rates near 6.43 percent, every penny counts. You need a strategy that bypasses the corporate fluff and puts money back in your wallet immediately.

We know the struggle. High monthly payments and the complex NAR commission rules make home buying feel like an uphill battle. You want transparency and tangible results. This guide promises to show you exactly how to stack these two financial tools to lower your effective purchase price. We will break down the 2026 conforming loan limits, the IRS rules that make rebates tax-free, and the specific concession caps for FHA and VA loans. It is time to pull back the curtain on the industry. Get ready to take control of your transaction and maximize your savings.

Key Takeaways

- Master the post-2024 NAR settlement landscape to turn agent commissions into a powerful negotiation lever for your next home purchase.

- Compare the mechanics of a realtor rebate vs seller concessions utah to decide whether you need immediate closing cost relief or a stronger, more competitive offer.

- Discover why agent rebates are often superior to concessions because they do not reduce the seller’s net profit, making your bid stand out in a crowded market.

- Learn the essential steps to secure your buyer rebate agreement in writing before you begin touring properties or researching local listings.

- Find out how to stack a buyer rebate of up to $5,000 with seller credits to effectively slash your purchase price and minimize your out-of-pocket expenses.

Financial Incentives in the 2026 Utah Housing Market

The old way of buying a home in Utah is dead. Before August 2024, most buyers didn’t even think about agent commissions. The seller just paid it, right? Wrong. The NAR settlement changed the landscape forever. Now, who pays the agent is a central pillar of your negotiation. In 2026, buyers are more selective. They have to be. With statewide inventory at 6.2 months, we are deep in a buyer’s market. You have leverage. Use it.

Cash is the biggest hurdle for most families. High interest rates have made monthly payments a challenge, but the upfront “gap cash” is what often kills deals. You need to understand the difference between a realtor rebate vs seller concessions utah before you sign a single document. These aren’t just industry terms. They are your two best weapons for keeping money in your pocket. One comes from your agent; the other comes from the seller. Knowing how to stack them is the key to a savvy purchase.

The Post-Settlement Reality in Utah

You can’t even tour a home in Sandy or Provo without a signed buyer agency agreement. This contract is your first opportunity to save. It dictates whether your agent is a partner in your success or just another expense. Sellers are increasingly hesitant to offer traditional 3 percent commissions. Instead, they are leaning toward concessions. Why? Because concessions feel like a price adjustment. They help the seller’s “net” look better on paper. The MLS no longer displays commission offers, making direct negotiation the only way forward. This lack of transparency means you must be proactive.

Why You Need a Savings Strategy Before Touring Homes

Don’t wait until you find your dream home in Lehi to talk about money. Average sold prices in Lehi are hovering around $692,806. That requires a lot of liquidity. You need to calculate your “Gap Cash” immediately. This is the total amount needed for your down payment plus closing costs. It’s the real number that determines if you can actually close the deal.

Smart buyers talk to their real estate broker about incentives on day one. If your broker isn’t offering a rebate, you’re leaving money on the table. In high-priced counties like Salt Lake, where the median price is $620,000, a $5,000 rebate isn’t just a bonus. It’s a bridge to affordability. Understanding the trade-offs of a realtor rebate vs seller concessions utah is no longer optional; it’s a survival skill. Combining a rebate with seller-paid concessions can effectively lower your purchase price without the seller feeling the sting. This strategy makes your offer more competitive while protecting your bank account.

Realtor Rebates vs. Seller Concessions: What is the Difference?

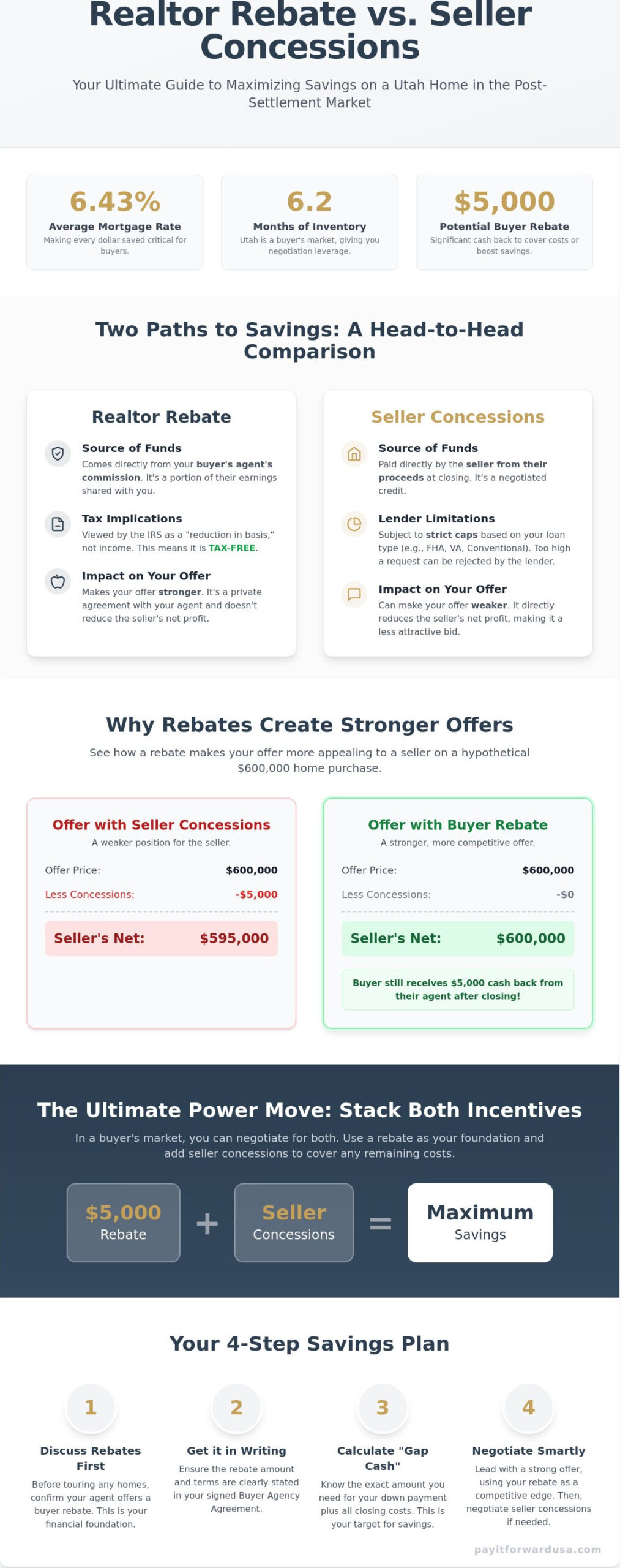

Stop overcomplicating your home purchase. To win in the 2026 market, you need to know exactly where your savings are coming from. The core difference between a realtor rebate vs seller concessions utah is the source of the funds. A realtor rebate comes directly out of your agent’s commission. It is their way of sharing the “paycheck” they receive for representing you. In contrast, seller concessions come out of the seller’s net proceeds. They are a credit given by the owner to help you cover the costs of the transaction. One is a professional courtesy from your broker; the other is a negotiated price adjustment from the seller.

Are these tools legal? Absolutely. Utah Administrative Code R162-2f-401l explicitly permits these financial inducements as long as they are disclosed. The Department of Justice even champions realtor rebates because they drive down costs for consumers. You aren’t bending the rules. You are playing the game like a pro. Both tools serve the same ultimate goal: reducing the amount of cash you need to bring to the closing table.

How a Utah Home Buyer Rebate Works

The mechanics are simple and powerful. When you close on a home, the listing brokerage pays your agent’s firm a commission. If you have a rebate agreement, your agent then passes a portion of that money to you. This is often handled as a credit on your settlement statement, effectively wiping out your closing costs. Because the IRS views this as a “reduction in basis” rather than taxable income, you don’t have to worry about a surprise tax bill. Using a Utah home buyer rebate is the smartest way to ensure you walk away with extra liquidity without needing the seller’s permission.

The Mechanics of Seller Concessions

Seller concessions are handled during the offer stage. You negotiate these credits directly within the Utah Real Estate Purchase Contract (REPC). These funds typically cover title insurance, appraisal fees, or even interest rate buy-downs. However, you must respect lender limits. For a primary residence with a down payment under 10 percent, conventional loans usually cap concessions at 3 percent of the purchase price. FHA loans allow up to 6 percent. If you ask for more than the lender allows, that extra money simply stays with the seller. Don’t leave money on the table. If you want to maximize your financial strategy, look into how a buyer rebate up to $5,000 can fill the gaps that seller concessions might leave behind.

The Comparison: When to Choose a Rebate over a Concession

Choosing between a realtor rebate vs seller concessions utah isn’t just about the math. It’s about strategy. You need to know which tool to swing and when. A seller concession is a direct hit to the seller’s bottom line. If you ask for $10,000 in credits, the seller sees their profit drop by exactly $10,000. In a competitive market, that could get your offer tossed in the trash. A rebate is different. Since it comes from your agent’s commission, it doesn’t affect the seller’s net proceeds at all. Your offer looks “cleaner” and more attractive while you still secure the cash you need.

Scenario A: The Cash-Strapped Buyer

If you are tight on liquid cash, prioritize seller concessions. They are the fastest way to reduce your “Cash to Close” at the settlement table. In competitive areas like Saratoga Springs, where multiple offers are still common, you might use these concessions for a permanent interest rate buy-down. This drops your monthly payment for the life of the loan. With average 30-year fixed rates around 6.43 percent, a 1 percent buy-down can save you hundreds of dollars every single month. It’s a long-term play for monthly affordability.

Scenario B: The Savvy Investor

Investors focus on the “cost basis” of the property. A rebate is superior here because it effectively lowers what you paid for the asset without requiring a lower appraised value. If a seller refuses to budge on price or concessions because they think their home is worth every penny, don’t walk away. Use your agent’s rebate to bridge the gap. This keeps the deal alive and your ROI high. If you are also planning to sell a property to fund your next move, check out our monthly MLS listing plan to save even more on the sell-side. Balancing a realtor rebate vs seller concessions utah is how you win the game of real estate equity in 2026.

Negotiating Incentives in your Utah Real Estate Contract

The contract is where your strategy becomes reality. You can’t just hope for a good deal; you have to write it into existence. When balancing a realtor rebate vs seller concessions utah, the paperwork is your most powerful tool. If your agent isn’t aggressive about these sections, you are leaving thousands on the table. Follow these four steps to lock in your savings before you sign on the dotted line.

- Step 1: Secure your Utah home buyer rebate agreement in writing with your broker first. This must be done before you submit an offer to ensure the lender can include it in your initial disclosures.

- Step 2: Research the seller. Are they using a flat fee MLS Utah service? Sellers using these low-cost models are often more price-sensitive but may have more room to negotiate concessions because they aren’t paying a traditional 3 percent listing commission.

- Step 3: Draft the REPC with surgical precision. Section 2 is where you define the seller’s contribution.

- Step 4: Balance the math. If you need a 3 percent concession but the market is tight, consider offering a slightly higher purchase price. This keeps the seller’s net profit high while keeping your cash in your pocket.

Using the REPC to Your Advantage

Section 2.1 (c) of the Utah Real Estate Purchase Contract is your best friend. Don’t use vague language. Use specific phrasing like: “Seller agrees to pay $X,XXX toward Buyer’s loan closing costs, settlement fees, and interest rate buy-downs.” If you are asking for high concessions, be wary of the appraisal gap. If the house doesn’t appraise at the higher price used to “roll in” your concessions, the deal could fall apart. Always keep your lender in the loop. If you negotiate $10,000 in concessions but your actual closing costs are only $8,000, that leftover $2,000 usually goes back to the seller. Don’t let that happen. Plan ahead to use every penny.

Common Pitfalls to Avoid

The biggest trap is the “Lender Limit.” For a primary residence with less than 10 percent down, conventional loans often cap concessions at 3 percent. FHA allows 6 percent; VA allows 4 percent. If you negotiate a deal for a realtor rebate vs seller concessions utah that exceeds these limits, you lose. The excess money doesn’t go to you; it stays with the seller. Timing is also critical. Your rebate must be disclosed on the Settlement Statement (Closing Disclosure). If it’s a surprise at the 11th hour, it can delay your closing. Finally, be careful with non-refundable deposits. If you’ve put down a large “due diligence” fee, you have less leverage to ask for concessions later if the inspection uncovers issues. Ready to take the first step? Go ahead and secure your $5,000 rebate today.

Maximize Your Savings with Pay It Forward Realty LLC

Don’t leave your financial future to chance. You’ve mastered the difference between a realtor rebate vs seller concessions utah. Now, it’s time to execute. Most brokers keep the entire commission for themselves. We think that’s outdated. At Pay It Forward Realty LLC, we put the power back in your hands. Our Buyer Rebate of up to $5,000 isn’t just a perk. It’s a fundamental shift in how Utah real estate works. We combine this rebate with expert-level negotiation for seller concessions to ensure you walk away with the maximum amount of cash possible. Why settle for one when you can have both? Balancing a realtor rebate vs seller concessions utah is the smartest way to win in 2026.

A strong offer starts with a solid foundation. Our affiliation with True North Mortgage provides you with free prequalification. This makes your offer stand out in competitive markets from Saratoga Springs to Salt Lake. When a seller sees you’re prequalified and represented by a rebate-friendly broker, they know you’re a savvy buyer. You get the leverage of a professional investor and the support of a local ally. No corporate stiffness. Just results. We’re here to strip away the unnecessary barriers that stand between you and your new home. Pay It Forward Realty LLC prioritizes your bottom line above industry tradition.

How to Claim Your $5,000 Rebate

The process is simple and direct. Connect with Kurt Mathewson, our Principal Broker, to discuss your specific goals. There’s no obligation. We want you to have the facts before you even step foot in a house. We help you understand the current inventory and identify where you have the most leverage to ask for extra concessions. When you close, your rebate is paid directly at the closing table. It appears right on your settlement statement as a credit toward your costs. It’s your money. You should keep more of it. We make sure the math works in your favor from the very first tour.

Full Service, Better Value

Some buyers think a rebate means fewer services. They’re wrong. You get full-service representation in Eagle Mountain, Herriman, Orem, and beyond. We pull back the curtain on the industry to give you total visibility into every step of the transaction. You get the expertise of a seasoned pro without the traditional high costs. We handle the REPC drafting, the appraisal gaps, and the tough conversations with listing agents. It’s a modern, streamlined way to buy. Stop overpaying for the status quo. You deserve a broker who is genuinely invested in your personal success and financial freedom.

Take control of your home-buying journey. Get your $5,000 Utah Home Buyer Rebate started today!

Take Command of Your Utah Home Purchase

Why leave money on the table when you can put it back in your bank account? Principal Broker Kurt Mathewson is ready to help you navigate these complex rules with total transparency and zero corporate fluff. We don’t just show houses; we engineer better financial outcomes for families across the Wasatch Front. Strengthen your offer today with a free mortgage prequalification through True North Mortgage. It’s time to stop following outdated industry norms and start making the market work for you. You have the tools, the strategy, and a bold ally in your corner.

Claim Your $5,000 Utah Home Buyer Rebate Now

Your path to a savvy purchase starts with one bold move. Let’s get you into your new home with more cash and less stress!

Frequently Asked Questions

Is a real estate commission rebate legal in Utah?

Yes, commission rebates are fully legal in Utah. The practice is governed by Utah Administrative Code R162-2f-401l. This rule allows for gifts and inducements as long as they are disclosed to all parties in the transaction. You must ensure your lender is aware of the rebate to avoid any issues with loan underwriting. Disclosure is the key to keeping your transaction smooth, legal, and compliant.

Do I have to pay taxes on a Realtor rebate?

You typically won’t pay income tax on a Realtor rebate. According to IRS rulings, a rebate is considered an adjustment to the purchase price of the home. This effectively lowers your “cost basis” rather than counting as taxable income. You don’t need a 1099 for it; just keep your settlement statement for your tax records. It is a win for your wallet and your tax bill.

What is the maximum seller concession allowed in Utah for 2026?

Maximum concessions depend on your loan and down payment. For primary residences in 2026, conventional loans allow 3 percent with less than 10 percent down, 6 percent for 10 to 25 percent down, and 9 percent for 25 percent or more. FHA loans are capped at 6 percent, while VA loans have a 4 percent limit. Always verify these specific caps with your lender before drafting your final offer.

Can I use a rebate for my down payment?

No, you cannot use a rebate for your down payment. Lenders require that your minimum down payment comes from your own verified, seasoned funds. However, a rebate is perfect for covering closing costs, title insurance, and prepaid items. This strategy frees up your other cash to be used specifically for the down payment requirement. It is about moving money to where it helps you most.

How do I ask for seller concessions without weakening my offer?

The best way to ask for concessions is to focus on the seller’s “net” proceeds. If you need $10,000 in credits, consider raising your offer price by that same amount. In a market with 6.2 months of supply, Utah sellers are increasingly flexible. Understanding the balance of a realtor rebate vs seller concessions utah allows you to stay competitive while protecting your liquid cash for other expenses.

Can I get a rebate if I am buying a new construction home in Utah?

Yes, rebates are often available for new construction. Most Utah builders pay a commission to buyer’s agents who represent clients in their communities. The key is to have your rebate-friendly agent accompany you on your very first visit to the model home. If you register without an agent, the builder may refuse to pay the commission that funds your rebate. Don’t walk in alone and lose your savings.

What happens if the seller concessions exceed my actual closing costs?

Excess concessions are lost to the seller. You cannot receive cash back from seller credits that exceed your actual closing costs. If you find yourself in this situation, ask the lender if you can use the extra funds to buy down your interest rate permanently. This ensures every dollar you negotiated actually benefits your bottom line. Never leave money on the table that belongs to you.

How does the NAR settlement affect my ability to get a rebate?

The NAR settlement actually makes getting a rebate more straightforward. Since August 2024, Utah buyers must sign a written agreement before an agent can show them properties. This is your chance to negotiate your rebate amount on day one. It removes the guesswork and ensures your realtor rebate vs seller concessions utah strategy is locked in before you ever submit a formal offer. Transparency is now the standard.